Memphasys: From IVF Breakthrough to Recurring Revenue Machine

Memphasys (ASX: MEM) is attempting something many ASX biotechs promise but few deliver: a clean pivot from scientific validation to commercial execution. The company’s narrative has shifted decisively away from proving the science and towards proving the business model.

As director Marjan Mikel put it bluntly, the shift has been deliberate and recent: “we made [the strategy] very public in around about September, October of last year… to focus solely and wholly on the commercialisation” .

At the centre of the story is the Felix™ system, a sperm separation device that replaces decades-old centrifugation methods. The company positions it as the first meaningful advance in andrology workflows in over 40 years, combining electrophoresis and filtration to produce higher-quality sperm samples in roughly six minutes, versus up to 45 minutes using traditional methods .

That speed is not just a clinical curiosity - it is the economic hook.

The real product: cartridges, not consoles

From a commercial perspective, the real product is not the machine but the consumable cartridge. Each IVF or ICSI cycle requires one cartridge, turning every procedure into a revenue event.

Mikel is explicit about this distinction: “our business model is not selling a device… it’s selling a new sperm separation technique that requires a Felix cartridge to be used every single time” .

This “razor-and-blade” model is well-worn territory in medtech, but Memphasys is only now beginning to prove it works in practice.

The March quarter appears to mark a turning point. Revenue reached roughly $111,000 across multiple regions, including Japan, Europe and the Middle East, representing the first meaningful multi-market contribution .

More telling than the headline number is what sits underneath. As Mikel noted: “we are getting repeat orders from existing clients… which is where our business model is built” .

From trial to workflow adoption

That distinction matters. Early-stage medtech stories often stall at the “trial phase”, where promising technology fails to embed into everyday workflows. Memphasys is arguing that hurdle has been cleared.

Clinics are not just testing Felix; they are incorporating it into standard operating procedures. In Mikel’s words: “we are getting involved in the workflows of these organisations… and that’s really important” .

The company’s commercial strategy has been reset accordingly. Gone is the diffuse R&D focus; in its place is a tightly defined go-to-market approach centred on direct engagement with IVF clinics and carefully selected partners.

Management has explicitly rejected traditional catalogue-style distribution. As Mikel put it: “you just can’t put it on a catalogue and expect it to sell itself” .

Why clinics are buying in

The pitch to clinics is straightforward and commercially grounded. Felix reduces sperm preparation time from around 45 minutes to approximately six minutes, standardises outcomes and improves lab throughput.

In IVF labs, time quite literally is money. Faster processing means more procedures per day, which directly boosts clinic revenue.

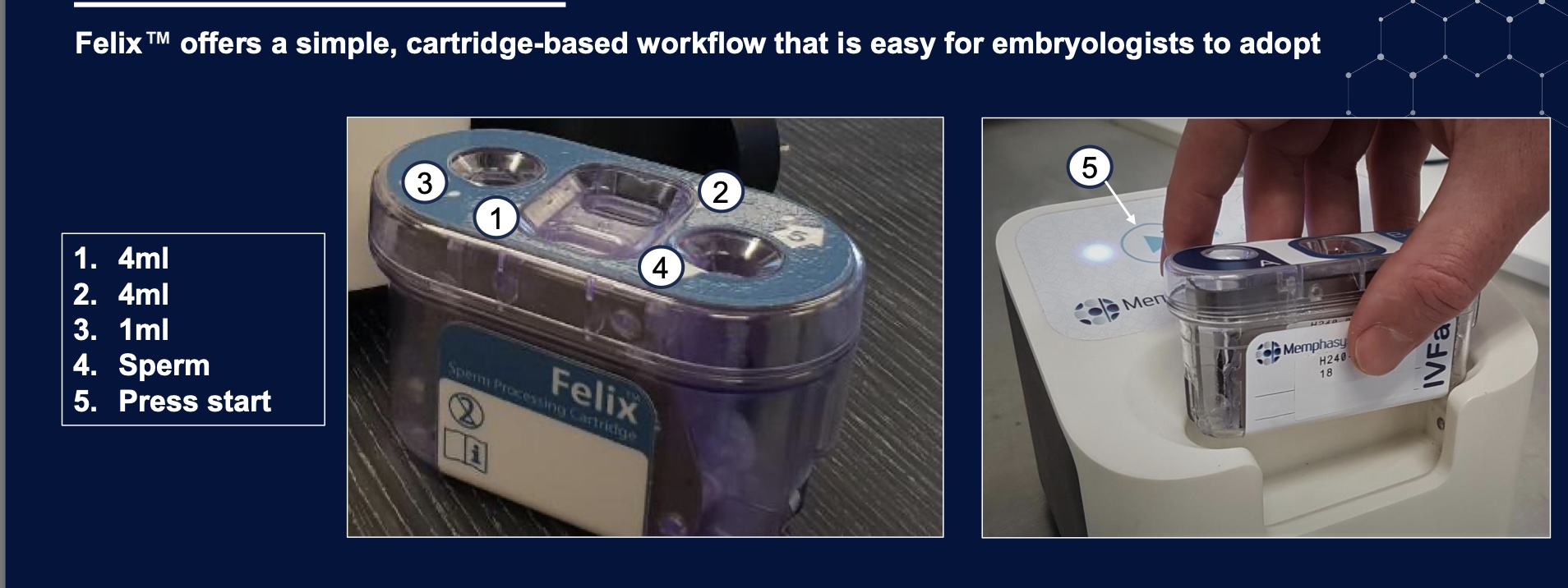

Mikel leans heavily on simplicity as the killer feature: “this is how easy it is… press button. That’s it” . He adds that even non-specialists can operate the system: “someone as dumb as me could do this… that’s how easy it is” .

The simplicity is not just anecdotal. As shown in the process diagram on page 12, the workflow is reduced to a handful of steps before activation, reinforcing how easily it integrates into lab routines .

Europe and MENA: where the growth lies

Geographically, Europe and MENA are the primary battlegrounds. Europe alone accounts for around one million IVF cycles annually, and the recently secured CE mark opens that market in full.

The company has already secured contracts in both regions and is seeing repeat demand. Mikel highlighted the significance of this early traction: “we’ve got contracts… and importantly, we are getting repeat orders” .

Japan provides a useful proof-of-concept market with ongoing repeat orders, but it is not the immediate focus. India, pending regulatory approval, represents a near-term expansion opportunity, while Australia and New Zealand are positioned as the next step following TGA approval.

The numbers start to stack up

The economics begin to look compelling when scaled. Management is targeting cartridge pricing of $80 to $150, with cost of goods below $40, implying gross margins above 60% .

Each clinic is expected to generate between $100,000 and $300,000 in annual revenue, depending on procedure volumes.

Mikel frames the model in simple, cumulative terms: “every single client builds on the previous clients… it’s a recurring revenue stream” .

This is where the leverage lies. Each new clinic does not replace revenue - it stacks on top of it.

Scaling brings its own challenges

Of course, early commercialisation is rarely smooth. Revenue remains somewhat lumpy as orders are shipped in batches, and scaling manufacturing to meet demand will require capital.

In fact, demand may already be testing capacity. Mikel was unusually candid on this point: “we are going to have to raise capital… because we’re selling too much Felix” .

That funding, however, is framed as growth capital rather than survival capital, with options ranging from debt to order-backed financing.

A large and growing market backdrop

The broader market backdrop is supportive. Global fertility rates are declining, and assisted reproductive technologies are a growing industry, forecast to expand significantly over the next decade .

Male infertility accounts for a substantial portion of cases, and the lack of innovation in sperm preparation techniques provides a clear opening for disruption.

As Mikel summarised: “there is no shortage of opportunity… every cycle is more revenue for us” .

The inflection point

Memphasys now sits at an inflection point rather than a destination. The technology case appears largely settled; the commercial case is just beginning to take shape.

The key question is whether early signs - repeat orders, multi-market revenue and contracted agreements - translate into sustained, scalable growth.

Mikel’s definition of success is tellingly operational: “broadening the number of clients… and making sure that they are reordering Felix on a regular basis” .

If that plays out, the story shifts from speculative biotech to a medtech platform with annuity-style revenues. If not, it risks joining the long list of promising technologies that never quite made the leap from lab bench to balance sheet.